Follow on Google News

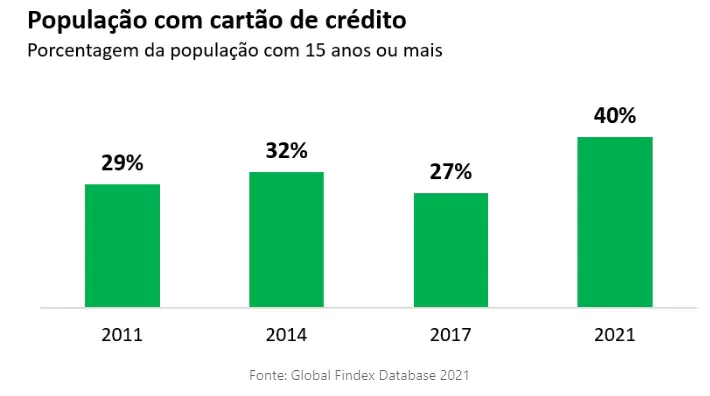

Today, a few decades after the first cards were launched in the second half of the 20th century, they are part of the daily lives of millions of consumers around the world - and in all income brackets. Data from Global Findex 2021 show that, on average worldwide, 24% of the population over the age of 15 has a credit card. In Brazil, this percentage reached 40%, after a jump compared to the 2017 figure (27%).

The aim of this article is to contextualize the advance in the use of credit cards in the individual segment, to discuss the profile of the use of this instrument based on a survey published by the Central Bank of Brazil and the implications of access to this type of credit on consumers' financial health.

The information released last Banking Economics Report, The study by the Central Bank shows an interesting scenario in Brazil: in June 2022, the 190.8 million cards issued represented almost double the economically active population, estimated at 107.4 million.

The growth in access to credit cards in Brazil comes against the backdrop of the recent performance of payment institutions in this segment, as well as the impetus given by the pandemic and the growth of e-commerce, a modality in which the payment process can be facilitated with the use of cards.

The analysis published by the Central Bank also shows that between 2019 and 2022, the percentage of users with more than one credit card rose from 38% to 46%. To confirm the hypothesis that having more than one card would be related to a need to increase the credit limit, the study cross-referenced the number of cards with the average balances used and found that, in fact, the greater the number of links, the greater the use of card balances. The result, as the report itself points out, suggests that taking out an additional card is aimed at expanding spending capacity, rather than the possibility of taking advantage of loyalty programs and benefits.

Credit cards have a dual function: as a payment instrument, when used in the “cash” function, and as a post-paid credit instrument, in installments subject to interest charges. Exploring this difference, the study found that among consumers with more than one card, the percentage of the balance used for purchases made on the card with interest charges increases compared to consumers with just one card. “This result suggests a trend towards the use of more expensive types of credit card as more links are added,” the study notes.

The point of attention when taking out several cards arises when the sum of the limits obtained from various financial institutions exceeds the consumer's ability to pay, and yet they continue to use the card beyond what their income allows. A survey carried out by the credit bureau sector showed that 31% of negative consumers reported that the reason for being negative was credit card arrears, followed by loans and credit cards.

In fact, late payment of credit card bills can be very costly. According to information from the Central Bank itself, the average interest rate charged by the revolving credit card reached an expressive 455% per year in May 2023.

According to data from the Central Bank, in June 2023, according to Free resources - Balance by type - Individuals, revolving and installment credit cards accounted for 7.4%, up 0.8% in 12 months.

In Free Resources - Delinquency by modality - Individuals (%), also in June 2023, the total individual credit card delinquency was 8.7%, up 1.7% in 12 months.

bureaus prevent this situation from worsening by offering comprehensive credit assessment tools that consider various relevant databases of borrower behavior and build bridges between creditor and debtor, facilitating the identification of overdue debts; credit assessment; the negotiation process between the parties; and credit recovery.

Consumers who are more prone to impulse purchases should reflect on the accumulation of cards and the importance of maintaining a credit limit compatible with their financial reality, thus inhibiting any excesses. On the other hand, it is up to financial institutions to set credit limits, especially for customers who already have approved limits at other institutions. The advance of financial inclusion and access to products such as credit cards is positive and should be welcomed. The evidence shows the need for financial education so that consumers and companies can exercise financial citizenship, avoid the risk of over-indebtedness and guarantee the sustainability of credit, thus stimulating the economy and social welfare.

Thanks for reading! Access other content at ANBC website.

President of ANBC - National Association of Credit Bureaus. Representative of Latin America in the World Bank Credit Committee. He also represents Brazil and Latin America in credit organisations accross the world, such as ACCIS, BIIA and ALACRED.