Follow on Google News

Owning their own home is undoubtedly the greatest dream of Brazilians. According to the Datafolha Institute, 87% of Brazilians share this feeling.

If the realization depended solely on one's own resources, many people would only achieve this dream after many years of saving. Home loans are there to help bring this dream forward.

This type of credit has very specific characteristics. In general, real estate financing involves amounts that go far beyond the family income and extend over many years. The term of the operations makes it challenging to raise funds to make them viable, given the credit risk and the risk represented by inflation.

In the case of Brazil, an important milestone in unlocking the real estate loans was the creation, in 1964, of the Housing Finance System (SFH). Still in force today, this system is designed to promote the construction or purchase of housing, with an emphasis on the lower income classes. Before the SFH was created, there was no structured system to connect the demand for and supply of real estate credit, even with the ongoing urbanization process.

The financing limit under the SFH is R$ 1.5 million. The interest rate is regulated, with the effective cost limited to 12% per year and the possibility of monetary correction of installments and balances. The funds used to finance the SFH come from two sources: voluntary, associated with deposits in savings accounts; and compulsory, associated with the Severance Indemnity Fund (FGTS).

However, there was still a part of the demand for real estate credit that needed to be met. This is how the Real Estate Financial System (SFI) came about, a parallel and complementary system to the SFH. The SFI was created in 1997 to meet the demand for higher-value real estate financing, and also focused on commercial real estate developments.

In the Real Estate Financial System, funds are raised through voluntary savings and the issue of debt securities, at freely agreed rates. In debt issuance, also known as securitization, debts are transformed into negotiable securities and offered to investors. When an investor buys one of these securities, the original creditor obtains more resources for new financing.

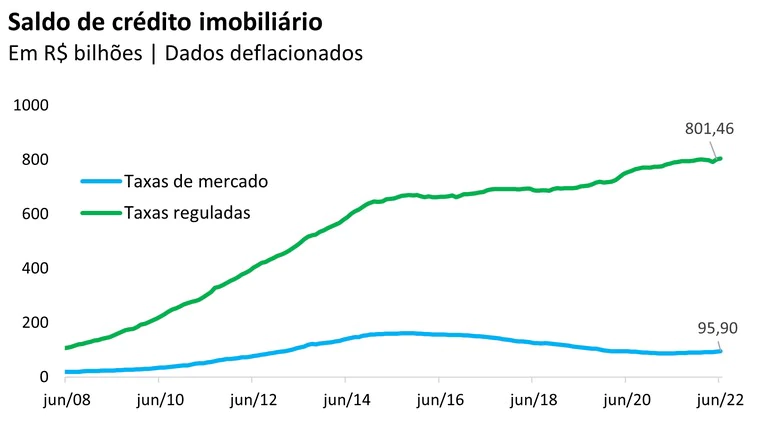

The graph below shows the evolution of real estate credit in Brazil since 2007. The data shows accelerated growth in real estate loans with regulated rates. The pace of growth began to slow from the beginning of 2016, in a context of severe economic crisis. Real estate loans with rates set in the market grew until the beginning of 2016, but then began to fall back.

A look at international experience can be useful in analyzing the Brazilian experience. In the USA, for example, mortgages are very popular instruments for acquiring homes. real estate. In this type of contract, the property is given as collateral for the financing, but remains the property of the borrower. This allows the same property to guarantee more than one credit operation.

Here, fiduciary alienation is more common. In this model, the financed property can be used while it is being paid for, but remains the property of the creditor until it is paid off, which reduces the bureaucratic process of enforcing the guarantee if the debtor becomes insolvent. This reduction in the cost of enforcing the guarantee makes it possible to reduce interest rates. An important instrument in real estate credit, fiduciary alienation can also be done with other assets.

The 2008 financial crisis is the best example of how the neglect of risk can contaminate the entire economy, producing damage instead of gains. The basic diagnosis of this episode in economic history puts the granting of credit to households without solvency capacity - the so-called "subprime" - at the root of the collapse of the financial system.

When looking for a mortgage, consumers will realize that one of the steps in the contracting process will be to consult the credit bureaus. This is how the sector contributes to the realization of a dream so dear to Brazilians: by offering stability to the financial system, so that the credit base can grow safely.

Thanks for reading! Access other content at ANBC website.

President of ANBC - National Association of Credit Bureaus. Representative of Latin America in the World Bank Credit Committee. He also represents Brazil and Latin America in credit organisations accross the world, such as ACCIS, BIIA and ALACRED.