Follow on Google News

With an eye on inflation expectations and the behavior of the dollar, the Central Bank's Monetary Policy Committee (COPOM) increased the prime rate by 0.75 percentage points. As a result, the SELIC rate went from 2% a year to 2.75%. This was the first increase in six years. If we go back six years, we'll find the country living with a double-digit prime rate: 14.25% per year. It was the old normal.

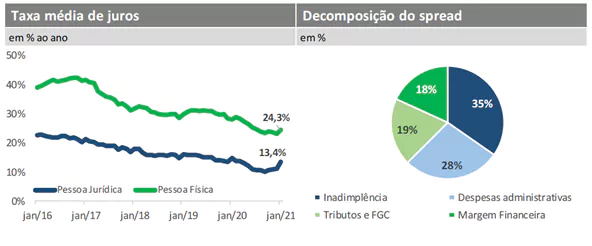

In line with the fall in the SELIC rate, interest rates for companies and consumers have also fallen. According to Central Bank data, the average interest rate for individuals reached a peak of 42.3% per year in the final months of 2016, falling to 24.3% in January 2021. The average interest rate for legal entities reached 22.2% per year in mid-2016. Today, it stands at 13.4%.

Since 2016, the fall in basic interest rates has been around 80%, while the rates contracted at the top have fallen by almost half. Why, after all, do we have this asymmetry? The answer is that the cost of raising funds, expressed by the rate SELIC, is just one of the components of the cost of credit. Default, Taxes and administrative costs are other important factors in the formation of interest rates.

According to Central Bank Banking Economics Report, The cost of raising funds for loans represents around 35% of the cost of credit. After deducting this cost, we arrive at the concept of banking spread. According to the most recent data, the average banking spread on operations with free resources was 23.3% in January 2021. Default accounts for 35% of the spread, followed by administrative expenses (28%); tax costs (19%); and, finally, the financial margin (18%).

The fall of interest Monetary policy, in short, can only have an impact on the interest rates paid by consumers and entrepreneurs to a certain extent. The task of making the cost of credit lower requires a greater effort and must mainly target the risk of default; guarantees; and the notorious legal uncertainty - the before and after of contracting credit.

In 2019, the international comparison placed Brazil as the country with the second highest spread in the world, a long way from third place. World Bank data allow the comparison to 2019, but even though the spread fell in the atypical 2020, it's hard to imagine that the country's relative position is much better today.

The debate on this particular feature of the credit has been going on for a long time. More recently, the Brazilian Federation of Banks (FEBRABAN) updated the issue, proposing a technical discussion on the subject. The diagnosis of the banking sector was collected in a book, It was distributed free of charge to society. The first point highlighted by the Federation was macroeconomic stability, a necessary condition for interest rates to remain low.

The book also elucidates the impact of banking concentration and the sector's profitability on the cost of credit, often pointed out as the villains of the spread. The Febraban clarifies that, despite being concentrated, the Brazilian banking market is competitive. On profitability, the book argues that the banking industry's profits are in line with what is observed in the rest of the world, showing that the discussion is more complex than common sense might indicate.

Based on the Central Bank's breakdown of the cost of credit, the document chooses the default as the number one villain and points out some ways to mitigate this risk. Data from bureaus show just how big this problem is in Brazil. The number of consumers has remained above 60 million since March 2018, having reached a peak of 65.2 million in May 2020.

Some measures debated over the last few years have been put into practice, such as the changes brought about by the Positive data, the implementation of the electronic duplicate, the recognition of the Central Bank's autonomy and, soon, the Open Banking. Added to this, as we always remember, is the development of the market itself, with the emergence of lending platforms. peer to peer, the marketplaces and the growing application of technology to finance, which increases competition.

Other measures, however, still need attention. A academic literature identifies, for example, an “anti-creditor” bias in legal disputes, which weakens the position of contracts and guarantees. As we have already pointed out here, According to a World Bank study, the institutional factor is one of the main bottlenecks for access to credit in Brazil.

For the next few years, the maturing of the measures that have already been taken and those that are yet to come could improve the country's ranking in the cost of credit. Society's interest in the subject of financial education is another novelty of our time and a crucial vector for the development of the credit market, promoting conscious consumption and making it possible to improve credit operations and the sustainability of the economy.

Thanks for reading! Access other content at ANBC website.

President of ANBC - National Association of Credit Bureaus. Representative of Latin America in the World Bank Credit Committee. He also represents Brazil and Latin America in credit organisations accross the world, such as ACCIS, BIIA and ALACRED.