Follow on Google News

We're almost halfway through the year. Since January, a lot has changed, both in the global and domestic economic scenarios. The permanent revision of projections has proved necessary because it is impossible to predict some events that decisively change the trajectory of economic variables. This was the case with the shocks caused by the conflict in Eastern Europe.

“War delays recovery”. Thus latest report from the International Monetary Fund (IMF) summarized the outlook for the global economy. In this report, the institution's projections pointed to growth of 3.6% in world GDP in 2022 - in January, in the previous publication, the expected growth was 4.4%. This slowdown in activity tends to spread around the world through the commodities market, international trade and greater volatility in the financial markets.

A global inflation goes against the grain of economic growth. The general level of prices is rising as a result of the shock to commodity prices, especially energy and agricultural goods. The result is an increase in interest rates beyond the levels expected at the start of the year. For example, in the last 12 months in the United States, the consumer price index reached 8.6% (American inflation) and Germany 7.9% (German inflation). The injection of resources during the pandemic, the disruption of production chains, the war in Ukraine impacting food and energy have affected the economies of the so-called inflation-resilient countries.

In Brazil, inflation also gained strength. In the last 12 months, the IPCA has accumulated an increase of 11.73%, according to IBGE data. With the recent acceleration in prices, it is very likely that inflation will exceed the projections made at the beginning of the year, when a variation of around 5% was expected for 2022.

Unlike the rest of the world, however, Brazil has seen its economic growth forecast rise and unemployment fall. Growth expectations for the Brazilian economy at the start of the year were very low. In January, the IMF projected GDP growth of 0.3%. Now, the agency's forecast is for growth of 0.8%. Among the factors favoring Brazilian activity is the rise in commodities.

Against this backdrop, what can we say about the credit market? To address this issue, it's worth looking back. The balance of loans and financing grew considerably at the height of the pandemic, especially for companies. This was important in cushioning the impact of the crisis. More recently, the pace of growth in credit to legal entities has fallen, being offset by the expansion of credit to individuals.

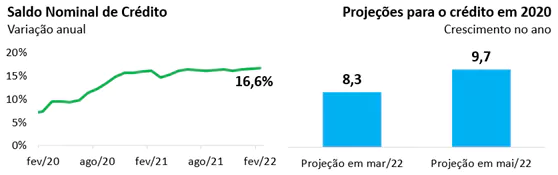

In December 2021, the expectations survey carried out by FEBRABAN pointed to growth of 8.3% in the National Financial System's total credit portfolio. In the most recent survey, carried out in May 2022, this projection was revised to 9.7%, with the expansion of credit to families expected to surpass that of the credit to companies. Credit balance growth is therefore expected to be above projected inflation, even in the face of rising interest rates.

This combination of high interest rates and credit expansion calls attention to a very important issue for credit bureaus: defaults. As we pointed out earlier, delinquencies remain at high levels. Higher interest rates mean larger installments in the budget of those who take out loans and financing, and this, in the absence of planning, tends to result in defaults.

The bureaus have warned of the risk of an increase in default throughout the year. The sector's baseline scenario is that the volume of people in default, currently at more than 60 million, will tend to grow in the coming months. The same is expected for the default rate calculated by the Central Bank. This reinforces the importance of credit analysis, using all the instruments that lenders have at their disposal today: credit score models, positive information, a negativity database and other relevant databases for credit assessment. Analyzing the payment capacity of consumers and companies is a fundamental premise for the functioning of the credit market and one that becomes even more important in times like these. Consumers need to be aware that rising prices are reducing their real income and interest rates are making it more expensive to take out loans and financing.

As this article has shown, we are always subject to uncertainty and scenario revisions. Some changes will be positive, others negative. The important thing is to strengthen the financial system, make it increasingly resilient to face shocks and, in the long term, contribute to economic development.

Inflation

Thanks for reading! Access other content at ANBC website.

President of ANBC - National Association of Credit Bureaus. Representative of Latin America in the World Bank Credit Committee. He also represents Brazil and Latin America in credit organisations accross the world, such as ACCIS, BIIA and ALACRED.