Follow on Google News

The announcement of the Safra Plan 2023-2024 was surrounded by great expectation. For months, the agricultural sector had been concerned about the limited supply of credit. At the end of June, the government presented the new Plan, setting the parameters for financing the sector's production over the next 12 months.

The justification for establishing these parameters, year after year, lies in the fact that agriculture and livestock account for an important contribution to the economy, with around 25% of GDP, and are subject to a wider range of uncertainties, such as adverse weather conditions. An unexpected drought, for example, could bring down the harvest. Crop plans subsidize the cost of financing these activities, sharing the inherent risks and making it possible to offer credit.

A Agriculture has been crucial in ensuring a good trade balanceIn addition to contributing to GDP growth. In the first quarter of 2023, the sector's GDP recorded a significant increase of 21.6% compared to the previous quarter, a result well above that seen in other sectors.

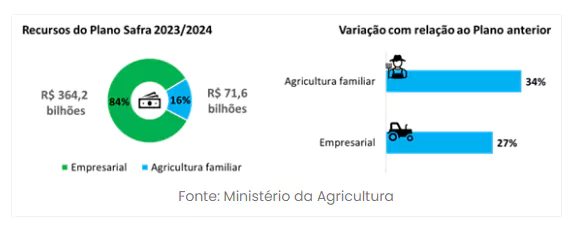

The volume of Crop Plan 2023-2024 grew. R$ 364.22 billion has been earmarked for medium and large-scale farming, marketing and investment, an increase of 27% on the previous plan. In addition to these resources, R$ 71.6 billion has been earmarked for family farming, an increase of 34% on the previous year. The interest rates announced in the Plan vary between 7% and 12.5% per year, depending on the purpose of the credit contract.

Like the Safra Plan 2022-2023, the current plan also seeks to promote sustainability. Rural credit and environmental preservation are more closely related than they might seem. One study released by the Climate Policy Initiative, from PUC-Rio, showed that an increase in the supply of credit in municipalities tends to increase productivity in agriculture, reducing the pressure for deforestation.

In addition to the indirect effect of the credit on environmental preservation, the Crop Plan 2023-2024 provides for a reduction of 0.5 percentage points in the interest rate for companies that are in compliance with the Rural Environmental Registry (CAR) analyzed, without any environmental liabilities. Producers will also be able to obtain a further 0.5 percentage point reduction if they adopt more sustainable practices, such as organic production, the use of bio-inputs and proper waste treatment, among others. The list of these practices is yet to be detailed.

Economic agents react to incentives. Raising funds, whether through bank loans or the capital market, has been used to make economic development and environmental preservation compatible. This movement is also encouraged by the private sector through ESG principles that direct capital market and credit resources to companies committed to the environmental and social agenda and good governance practices.

While the adoption of good environmental practices makes producers eligible for credit at lower interest rates, the adoption of environmentally damaging practices can be an impediment to contracting credit. Credit analysis still considers economic and financial criteria, but is increasingly incorporating social and environmental production criteria, based on the understanding that these risks can have financial impacts.

In addition to the negativity and credit history information that is essential for assessing the risk of default, the credit bureau industry is already working on developing models that assess socio-environmental risk in the agricultural sector. These tools will help distinguish producers, allowing financial institutions to provide credit on fairer terms, rewarding good payment history and good environmental practices.

The presence of sustainability in the latest crop plans shows, in short, a paradigm shift. Access to the credit market appears to be an instrument to encourage the adoption of sustainable and socially responsible practices, mitigating long-term risks that traditional credit analysis would be difficult to capture and making the Brazilian agricultural product more competitive on the international stage.

Thanks for reading! Access other content at ANBC website.

President of ANBC - National Association of Credit Bureaus. Representative of Latin America in the World Bank Credit Committee. He also represents Brazil and Latin America in credit organisations accross the world, such as ACCIS, BIIA and ALACRED.