Follow on Google News

History shows that, over the centuries, humanity has sought to improve the process of exchange, and this has been decisive for economic development. From barter to fiat currency, many stages have been covered. This trajectory is demonstrated in Credit Timeline, published by ANBC, which takes us back to ancient times. More recently, technological advances have led to new transformations in payment methods and solutions that didn't even exist a few years ago, but have quickly been incorporated into the daily lives of consumers and companies.

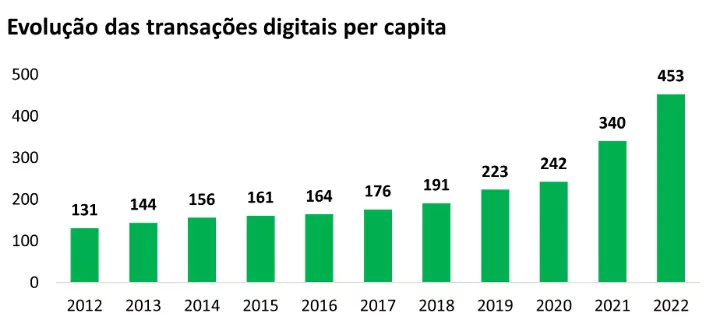

Data available on Banking Economics Report (REB) 2022, of Central Bank, These figures indicate the stage of this transformation in Brazil. The number of digital financial transactions per capita per year has grown significantly over the last decade, from 131 in 2012 to 453 in 2022.

The survey considered the following modalities: bank balance transfers; credit, debit and prepaid cards; PIX; boleto; and automatic debit. Over the last ten years, it is possible to distinguish between two periods. From 2012 to 2017, the use of these instruments increased. Since then, this growth has accelerated. In addition to the technological vector, other factors have contributed to this result: the regulatory update, which allowed, for example, the emergence of payment institutions, and the psychosocial factor, especially since the Covid-19 pandemic.

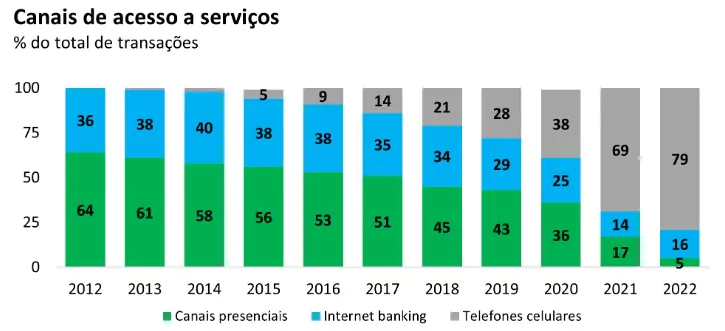

The study also confirms the growing importance of cell phones, which, according to the Central Bank, would characterize a new phase of digitalization. In 2022, financial transactions via cell phones accounted for 79% of total transactions, while transactions via internet banking accounted for 16%. Only 5% of transactions were carried out through face-to-face channels. This is very different from 2012, when face-to-face channels accounted for 64% of all transactions, and cell phones were practically non-existent for this purpose.

If the cell phone emerges as the main channel, the PIX has established itself as the main payment instrument in a short period of time. According to the figures presented by the study, PIX leads the way among the other instruments, with 29% of total transactions. This is followed by credit card (20%), debit card (19%) and boleto (11%), among other modalities.

On the other hand, the amount of cash withdrawals has been falling, suggesting a reduction in the use of cash. In 2012, around R$ 4.5 trillion was obtained through cash withdrawals; by 2022, this figure had fallen to R$ 2.1 trillion. “Cashless economy” is the term used to define the phenomenon of abandoning the use of cash and the growing adherence to digital forms of payment and transfer of funds.

This phenomenon can also be observed in other parts of the world, as noted by Bank of International Settlements (BIS) report, published in 2023. With data covering up to 2021, the report shows significant growth in digital means of payment, both in terms of the number of transactions and the amount transacted. The data for a group of 27 countries, including Brazil, China, the USA and Argentina, among others, shows that the number of transactions per capita per year will rise from 179 in 2012 to 332 in 2021. The same report points out, however, that the demand for cash remains relatively stable.

In addition to payments and transfers, the entire management of your financial life is now in the palm of your hands, speeding up the number of financial transactions, including credit. Credit bureaus have kept up with this movement by providing apps to access services such as making inquiries to credit bureaus to find out about any restrictions, accessing credit scores and proposing negotiations. In addition, there are a variety of apps to help you keep track of your finances on a daily basis.

Thanks for reading! Access other content at ANBC website.

President of ANBC - National Association of Credit Bureaus. Representative of Latin America in the World Bank Credit Committee. He also represents Brazil and Latin America in credit organisations accross the world, such as ACCIS, BIIA and ALACRED.